total loss frequency reached 22.8 percent through October 2025, up from 22.1 percent the prior year and on pace for a second consecutive record. Industry claims data had already put the broader collision total loss rate at 27 percent for 2023, and the numbers kept climbing through each reporting period after that as body shop labor rates pushed past 190 dollars an hour in many metro markets and the average age of the American car parc hit 12.6 years. Over 72 percent of total loss valuations now involve vehicles seven years old or older, and a vehicle that would have been repaired in 2019 at the same damage level gets written off today because the repair estimate crosses the threshold against a depreciated value that was already sitting closer to the line than it was five years ago. The salvage channel absorbing those declarations moves somewhere between 4 and 5 million vehicles a year, and what's coming through looks different than it used to. Hail totals, theft recoveries, and minor collision damage declarations have grown as a share of the inventory, meaning the salvage title lookup on a given vehicle increasingly returns a loss event that didn't involve structural compromise at all. Repairable appraisals for damages of 2000 dollars or less fell from 41.5 percent in 2019 to 25.5 percent through mid 2025. Higher deductibles are pushing that number down, and the shrinking low dollar repair pool pushes the total loss share up even without a change in crash severity.

The two dominant auction operators processed roughly 2.5 million vehicles in their most recent full reporting periods, selling as is with condition notes based on visual inspection and nothing else. The buyer's premium runs on a tiered scale from roughly 10 to 25 percent, depending on bid price, and a 10000 dollar bid costs something like 2000 to 2500 dollars in premium before transport, storage, or repair enters the picture. Cross country transport adds over 1000 dollars. Storage fees start once the free window closes. The gap between bid and actual acquisition cost is wider than most people expect, and the miscalculation usually happens before any work has started.

The threshold gap across states is what puts some of the better inventory at salvage auctions into the channel in the first place. A state with a 75 percent threshold declares a vehicle totaled when the repair cost exceeds three quarters of its pre loss value. A 90 percent threshold state won't total the same vehicle with the same damage. A vehicle worth 28000 dollars before a hailstorm, quoted at 21000 in paintless dent repair across several hundred dents, ends up declared a total loss in the lower threshold state, even though nothing mechanical is wrong with it. That vehicle can be a good buy if the vehicle history report is clean and the hail is the only damage event on the NMVTIS record. Shops have been known to inflate the dent repair quote to get the claim over the threshold, and auction history reports with prior appraisal values on file do catch that sometimes, though not reliably.

Front end hits are harder to price. How much damage is actually there depends on what the shop finds after teardown, and an estimate written before the vehicle is apart is never as solid as the number on a hail total, where everything is sitting on the outside of the car. A frame that went through hydraulic straightening doesn't come back to factory spec, full stop, and the crush zones are permanently compromised, no matter how clean the body looks. The NMVTIS record is what the bid should be based on. Title brand history from every state the vehicle was registered in, the ownership chain, salvage, and total loss designations. Odometer readings at each title event are in there, too. Fraud on salvage inventory odometers shows up when a reading drops between two events or makes a jump that doesn't line up with the calendar. Vehicles show up at salvage auction with a clean title in the selling state after being branded salvage in another state all the time, because not every state picks up the brand from the state that issued it. NMVTIS files on vehicles that moved through three states in under fourteen months, with no real reason for any of the transfers, will show the brand from the first state just gone by the time it reaches the last one. The 2025 flagged files showed the same thing, though that data only covers vehicles for which someone actually ran a check on. NHTSA recalls are a separate federal database, pulled by VIN, and completion rates on older models are low. An open recall on brakes or fuel system parts adds weeks and real cost to a build that is already behind.

The NICB put the flood damaged vehicle count from the 2024 hurricane season at roughly 347000, mostly out of Florida, the Carolinas, and Tennessee after Helene and Milton, and a lot of that was still in resale and retitling channels into 2026. Hurricane Erin hitting Category 5 in August 2025 and pushed coastal flooding from the Outer Banks into New Jersey, made the pipeline longer, and a record number of flash flood warnings through the summer nationally put more uninsured vehicles into the water damage pool that never shows up in the insurance system at all. Flood car history doesn't always cross state lines with the vehicle because not every state picks up the flood brand from the state that wrote it. The NICB data covers insurers writing about 88 percent of personal auto policies. The other 12 percent, and every uninsured vehicle that sat in floodwater, goes completely unrecorded. Water gets into harnesses, modules, and connectors, and none of it is visible at the time of sale. Something that drives fine on the lot starts throwing intermittent codes weeks later as corrosion works into the wiring. Fire does something different, but the end result is the same sort of problem, soot and combustion residue from burned interior materials coat the insides of module housings, and nobody sees it unless the units get pulled. The professional salvage buyers mostly stay away from flood and fire lots and leave them for rebuilders with real electrical diagnostic capability. The auction history on those vehicles usually tells the story, two or three failed sales before somebody finally takes the bid.

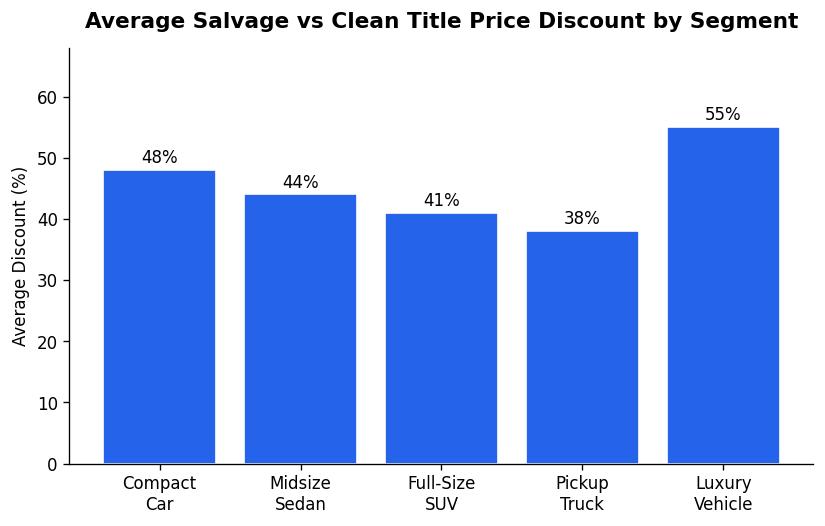

Title washing after a salvage auction and rebuilt title depreciation sits at roughly 25 to 40 percent below the clean title comparable value. It stays there. The repair quality doesn't matter, the paperwork doesn't matter, the discount is baked in. Underwriting and financing restrictions follow a rebuilt brand through every resale, and nobody prices around it. The math on a salvage buy runs against the rebuilt title comparable, not a clean title, and it has to cover bid plus premium plus transport plus repair plus inspection and registration before there is any margin. California's Bureau of Automotive Repair and similar programs in Texas, Florida, and a few other states run a VIN check across every physical VIN location on the vehicle, and that does catch some of the title fraud that uses the rebuilt designation to launder a bad history. Cross state registration is its own problem. Paperwork requirements differ everywhere and can hold up the rebuilt title by weeks, and that delay runs up storage on a vehicle that is not going anywhere.