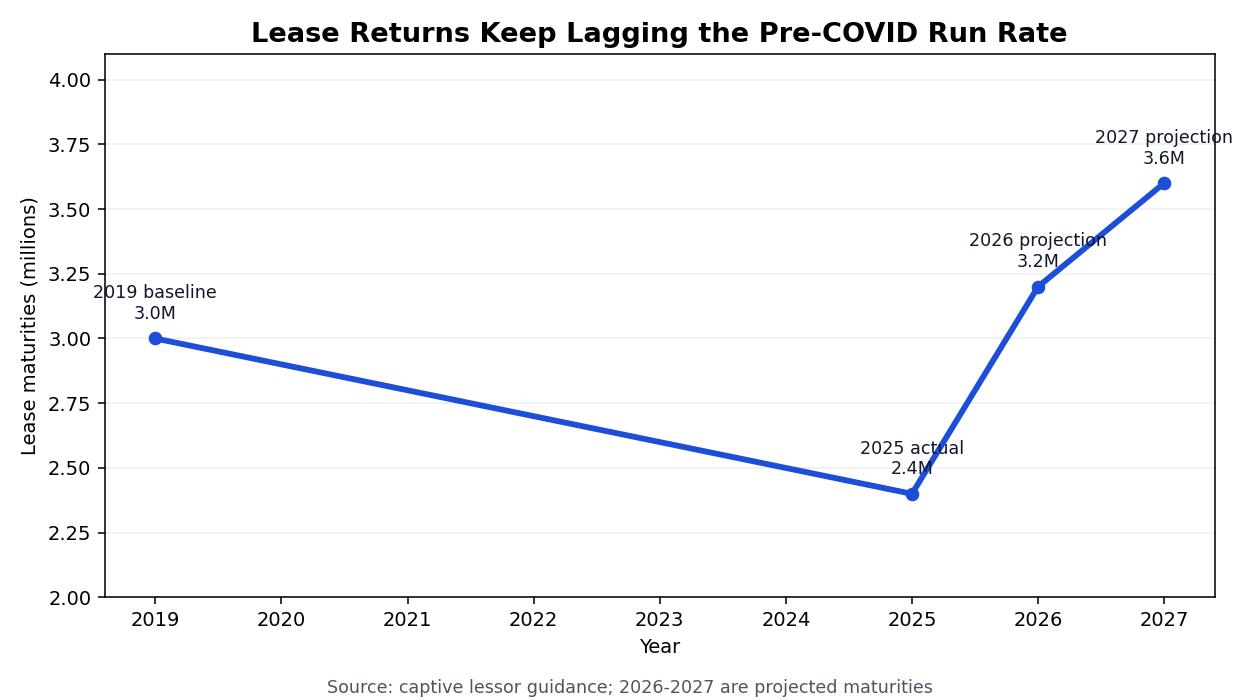

Roughly 2.4 million vehicles came off lease in 2025, a figure that flashed across a remarketing forecast deck last October and froze a room full of acquisition leads who remember when the pipeline cleared 3 million returns per year without anyone calling it a sourcing risk. Nobody working the lanes between 2015 and 2019 treated returning leases as fragile inventory; the stream was constant and the verification work was built for it.

Leasing still accounted for 32 percent of new retail transactions in 2019 with luxury penetration north of 50 percent and non luxury segments hovering around 26 percent. After March 2020 the origination spigot closed and stayed that way for almost five full model years, leaving average lease penetration at 22.8 percent between 2020 and 2024 and forcing every sourcing model that depends on institutional returns to get rewritten.

The cumulative shortfall for 2023 through 2027 against that pre-pandemic baseline sits near 11.7 million units, which is the number that ended up on a whiteboard in Dallas and stayed there while buyers processed what it meant. Those missing cars and trucks were supposed to enter wholesale with single-owner histories, low mileage, factory service documentation, and clean NMVTIS files. The leases never existed, so the documentation never existed either.

First-half 2025 maturities landed 41 percent below the prior year, erasing about a million units from what used to be peak sourcing season. Acquisition teams that rework their playbooks every quarter have already torn up three or four revisions in the past 18 months, and most expect the current version to hold only until late summer before another break in supply. NAAA houses still moved more than 8 million vehicles in 2025 and pushed total offerings to 12.3 million, but the conversion rate slipped to 58.5 percent even as in-lane averages climbed to about $13,800, so the spread between wholesale and retail stayed upside down for longer than anyone on the seasonal pricing circuit projected.

Run the math on a mid-price unit at a volume store in Georgia and the exercise leaves negative $800 in gross after transportation and recon, which is why multiple operators in different states independently described everyday sourcing as “broken.” Bread-and-butter inventory at the higher-volume rooftops now costs more to buy wholesale than it can return in retail gross, the kind of admission you only hear near the coffee urns at conferences, never on the keynote slide.

Acquisition records pulled from nine dealerships across four states last year make clear where the replacement inventory actually came from. Trade-ins at least provide a partial custody chain, but after that the picture drops off fast. Street purchases from private parties keep growing at every rooftop surveyed, consumer-facing buying platforms pick up another slab of the total, and dealer-to-dealer lateral trades cover the rest.

One sample of three Mid-Atlantic stores alone showed more than 500 checks a month going to private sellers, including a Roanoke buyer who met a customer in a grocery parking lot, handed over a cashier’s check, and accepted a hand-written disclosure showing 87,000 miles as the entire paper trail for a unit that retailed for $38,000 three weeks later. That is now ordinary.

A captive finance return on the same model year would have rolled back through a simulcast lane with a full custody chain, inspection photos, maintenance history back to delivery day, and a structured NMVTIS record covering every jurisdiction where the vehicle ever carried a title. That institutional trail is the piece the private-party pipeline cannot reproduce.

NMVTIS compliance data pulled last fall still showed 14 states allowing a dealer to close a retail sale without pulling the vehicle history report. Salvage branding rules in Ohio look nothing like the statutes in Alabama, flood damage definitions in Texas do not match the language in Pennsylvania, and there is no reconciliation layer between them. The same title-washing pipeline that has been tracked since 2018 now benefits from the fact that the dealer never saw the vehicle in an institutional lane in the first place.

Lending fraud exposure ran near $9.2 billion in 2025 even before you haircut the estimate, and more of those cases trace back to units acquired through private channels with little more than a driveway bill of sale. Tennessee keeps reappearing in odometer rollback filings, Montana follows closely on title anomalies, and both states still retitle vehicles with almost no verification against the original jurisdiction.

Before 2020 the workflow was upstream. Captive lenders ran the inspections, auctions generated condition reports, certified pre-owned programs pulled the full history, and the retail store received a unit that had already been documented. Now the dealer buys a car out of a driveway, runs the VIN check and the lien search or skips them entirely, and hopes the next owner never uncovers a gap.

Q3 2025 data put used-vehicle gross at 5.4 percent versus 7.3 percent in 2019, almost two full points of margin gone while the verification workload per unit moves in the opposite direction. One GM in North Carolina needed 15 units frontline-ready overnight last September and cut vehicle history reports out of the prep budget to hit the target. That decision is the opposite of what every VIN decoding guide tells buyers to expect.

Lease maturities might climb back to roughly 3.2 million units in 2026 and maybe 3.6 million in 2027, but battery-electric returns alone could spike 230 percent as the pandemic-era leases roll off. Residual analysts at two captive lenders admitted late last year that none of their current models actually price that volatility in, and the auction companies asked how they plan to document EV battery condition gave five different answers.

A dealer advisory board meeting in January put eight people at the table, and three openly said they run zero formal checks on privately sourced units. That admission hung in the air. Every month the lease pipeline stays below its old volume, another group of dealers fills the gap with inventory nobody verified, and it only takes one rolled odometer or scrubbed flood brand hitting the next transaction to unravel the entire custody record.