A year as volatile as 2025 turned out to be should have knocked the rebuilt title discount off its axis, but it did not, and frankly, that surprised more than a few people tracking salvage markets. The wholesale used vehicle index finished at 205.5, which was barely 0.4 percent above where it opened in January. Compare that to a longstanding annual average of 2.3 percent appreciation, and you are looking at a year that was functionally stagnant on net, though calling it stagnant understates how wild the middle months actually got. April alone saw the index spike to 208.2, the highest monthly print since late 2023, after 25 percent tariffs on imported vehicles and parts took effect, and wholesale buyers panicked their way through a 2.7 percent single-month price jump that nobody running a remarketing desk had budgeted for. Days supply fell to 41 from 46 the year prior, and the squeeze was worst in late model stock because lessees were not returning vehicles. Full year retail used vehicle sales came in around 20.4 million units, well past the 20.1 million forecast, so demand was not the problem. And rebuilt title pricing through all of this? Zero measurable response. The discount sat at 20 to 40 percent below comparable clean title retail all year, depending on segment, age, and loss event type, and the band did not waver by any meaningful margin.

Where does rebuilt inventory actually come from? Total losses, overwhelmingly, and 2025 produced them at a pace that even the people who track this data full time found startling. Through October, 22.8 percent of all physical damage claims were being totaled out, running 0.7 points ahead of the same window in 2024, which had itself been an all-time record year. Roughly 72 percent of those total loss valuations fell on vehicles seven years old or older, which is the exact age bracket where rebuilt title inventory concentrates and where the discount against clean title equivalents tends to run at maybe 20 to 25 percent rather than the wider 35 to 40 percent gap found on newer metal fresh out of insurance settlements. A comparison pulled from early 2025 auction records makes the point concretely. A seven-year-old midsize sedan, clean title, 85,000 miles, was wholesaling at $9,500 to $11,000, depending on condition and region. That same vehicle, carrying a rebuilt brand after a front-end collision repair, was clearing salvage auction at $6,500 to $8,000. That spread has not shifted by more than a few hundred dollars in three years running now, through tariff shocks and rate hikes and the entirety of the pandemic-era inventory distortion, because the mechanics holding it in place are structural. Carriers recover only what the total loss settlement allows at the salvage auction. Rebuilders will not touch a unit unless the margin between acquisition cost and retail clears labor and parts. Neither input cares about trade policy. For more on how total losses flow into the used car market without always getting properly flagged, see our coverage of total loss vehicles that never get branded.

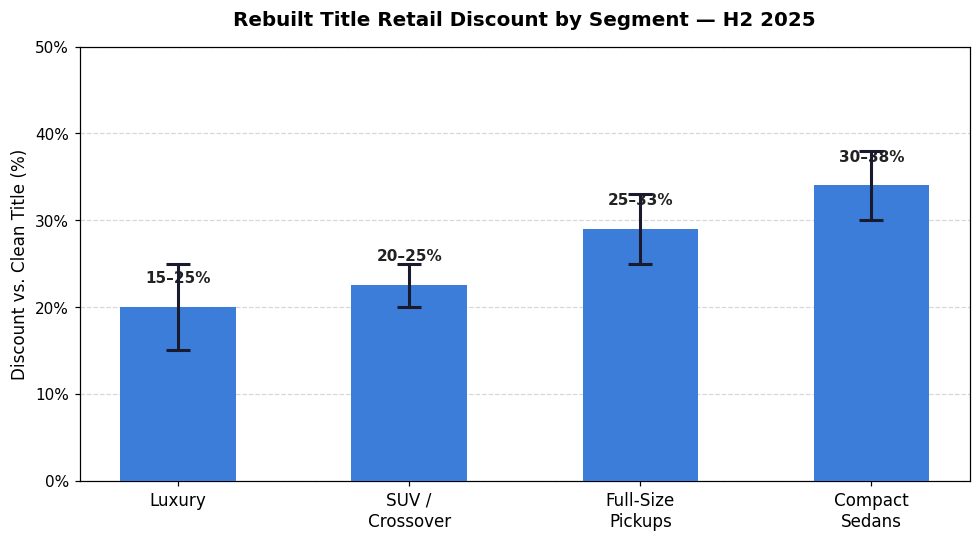

Wholesale data by segment told a messier version of the rebuilt discount story than the topline index let on. Luxury ran hot for five straight months into mid-2025 and posted 8.8 percent gains by June, which anybody watching lease returns could have guessed would happen once tariff anxiety started pulling transaction prices upward on new inventory. Sport utility was not far behind at 6.0 percent. Compact sedans, though, actually finished 2025 below where they had been the prior year, and full-size pickups barely moved, gaining under one percent through December. Salvage reserves and rebuilder acquisition costs follow the wholesale market, always have, so when clean title climbs, the rebuilt gap tightens, and when clean title stalls, the gap opens back up. Pull the second-half 2025 auction records on rebuilt sport utility vehicles and discounts to clean title were running 20 to 25 percent, which is noticeably compressed versus the 30 to 38 percent discounts on rebuilt compact sedans, where the clean title benchmark was going nowhere. Pickups ended up at 25 to 33 percent, about where you would expect, given that full-size truck wholesale spent all year caught between tariff exposure on the production side and seasonal depreciation rolling in during Q4. This kind of segment-level divergence is also visible in broader depreciation data across vehicle segments.

For anyone doing VIN check or vehicle history verification work, the volume side of 2025 probably matters more than what prices did. Total loss frequency was writing records all year and pushing units into salvage channels faster than any prior twelve-month stretch on file, and at least one major auction operator posted roughly 9 percent growth in domestic insurance consignment volume while average selling prices climbed 8.4 percent alongside it. Rising salvage prices ought to push rebuilder acquisition costs up and squeeze the rebuilt discount tighter against clean title, and in some segments, that is precisely what the data showed. Sport utility and crossover categories saw both inputs climbing in tandem through 2025. Compact sedans went the other way entirely. Clean title wholesale on compacts was flat to falling, and yet salvage acquisition costs kept drifting higher because rebuilders were competing harder for whatever rebuildable stock came through, so margins got thinner, and some shops just stopped bidding on units they would have grabbed twelve months prior. Marcus Hill, who supervises DMV enforcement in Arizona, mentioned that title brand applications for rebuilt sedans in the compact and subcompact categories fell about 15 percent year over year through September in his jurisdiction alone, a drop that lines up cleanly with what the margin data was telegraphing from the auction side. The mechanics of how rebuilt titles get applied at the state level are documented in our piece on how the rebuilt title brand differs by state.

Tariffs did not touch rebuilt title pricing directly, but they leaned on it sideways by making clean title used vehicles more attractive to a wider pool of buyers than usual. New vehicle transaction prices climbed through spring and summer, somewhere between $2,000 and $4,000 per unit on import-heavy segments, depending on who you ask, and that was enough to push displaced new car shoppers into used inventory and lift clean title retail, especially on sport utility and crossover stock. None of that demand bled over into the rebuilt title market. The financing wall, as it always does, held the line. Mainstream lenders still refuse to originate on rebuilt title paper, which is a fact that has not changed in decades and probably will not change next year either, so buyers in the rebuilt space pay cash or carry specialty notes at rates that exist in their own universe, regardless of what the federal funds rate or tariff schedule might be doing at any given moment. Rebuilt title pricing spent 2025 as its own island, tethered to the broader used vehicle market at the salvage auction level but otherwise walled off from whatever was happening at retail. That isolation is actually what makes the 20 to 40 percent band so reliable as a fraud detection benchmark in vehicle history report analysis. When a rebuilt title listing shows up priced well inside that expected discount against clean title comps, the explanation is almost never legitimate. It is either a pricing mistake or a title brand that is hiding damage the documentation should have surfaced, the same pattern documented in our piece on how auction records diverge from retail listings.